If you own or hold commercial property in the UK, the Jigsaw CVA judgment is the most important business rates ruling you will read this quarter. It lands at an awkward moment: two and a half weeks after the new 2026 rating list took effect, with new multipliers sharpening the cost of every void in the country, and it quietly closes one of the exit doors landlords have been nudging open for years.

Here is what the case says, and why it matters for the way you think about empty property risk.

The short version of the facts

Robinson Webster (Holdings) Ltd, the corporate parent of the Jigsaw fashion brand, entered a Company Voluntary Arrangement in August 2020. Under the CVA it agreed to “exit” its shop at 44 Bow Lane in the City of London, hand back the keys and offer to surrender the lease. The freeholder declined the surrender. The unit sat empty for three years. The City of London Corporation pursued Robinson Webster for more than £220,000 of unpaid business rates.

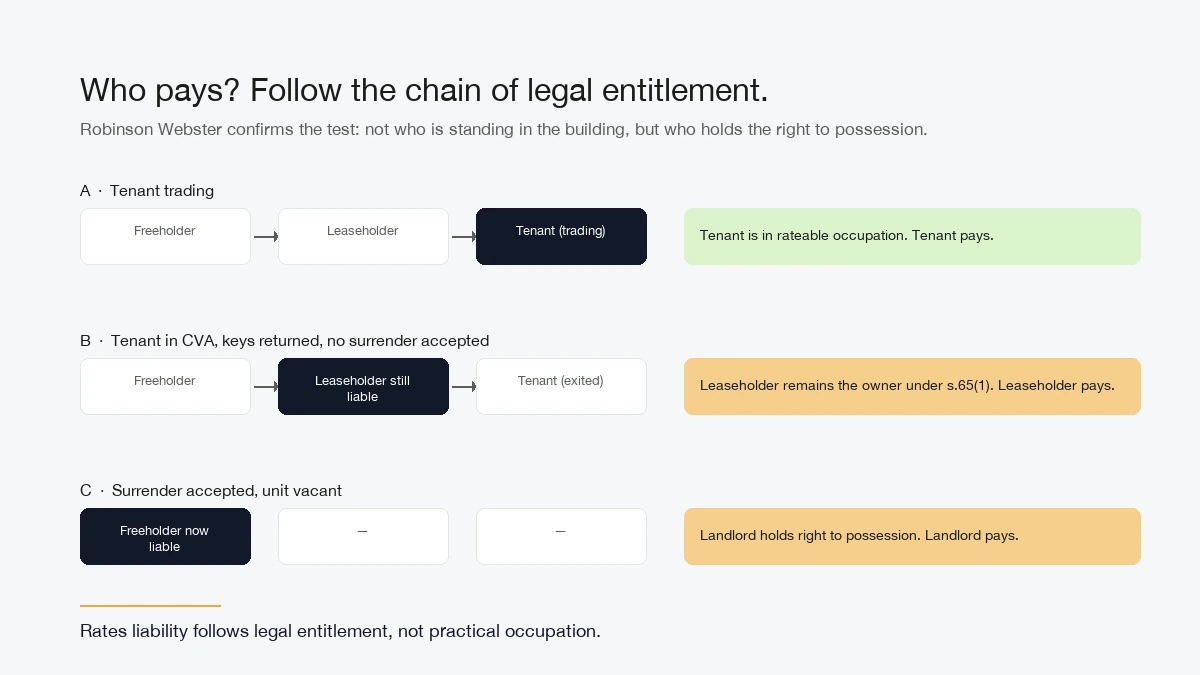

The High Court ruled for the billing authority. Because there had been no express or implied surrender, Robinson Webster remained the legal lessee and held the immediate right to possession. That made it the “owner” for the purposes of section 65(1) of the Local Government Finance Act 1988, and the liability order should have been made against it.

The legal principle you need to carry into 2026

Strip away the corporate detail and the rule is stark: rates liability follows legal entitlement, not practical occupation. It does not matter that Jigsaw had walked out. It does not matter that the shop sat dark for three years. What mattered was who had the legal right to possession at each point in time, and nobody had taken the keys back.

Rates liability follows legal entitlement, not practical occupation.

This is the same analytical frame the courts applied in Principled Offsite Logistics v Trafford in 2025. The law is converging on a clean rule: look at the paperwork, not the behaviour. Whoever sits at the top of the chain of legal entitlement pays.

For landlords, that cuts both ways.

The upside for landlords

The ruling does offer meaningful protection. Local authorities can no longer treat the landlord as the “better target” for rates simply because a tenant has gone into a CVA, administration or liquidation and stopped trading. If you have not accepted surrender, you have not taken possession, and you have not signalled possession resumption, you are not the statutory owner. You can tell the council exactly that, with Robinson Webster in hand.

That alone justifies an urgent review of your insolvency playbook. Any tenant headed into a formal process should be handled with the question “what does this do to rates liability?” treated as a first-order concern, not an afterthought.

The uncomfortable implication

The same rule that protects you when a tenant is insolvent hurts you when your property is simply empty. Once you are back at the top of the legal-entitlement chain, with no tenant between you and the valuation list, the liability sits with you by default. After the short three- or six-month empty relief window expires, every day of vacancy is a rates day.

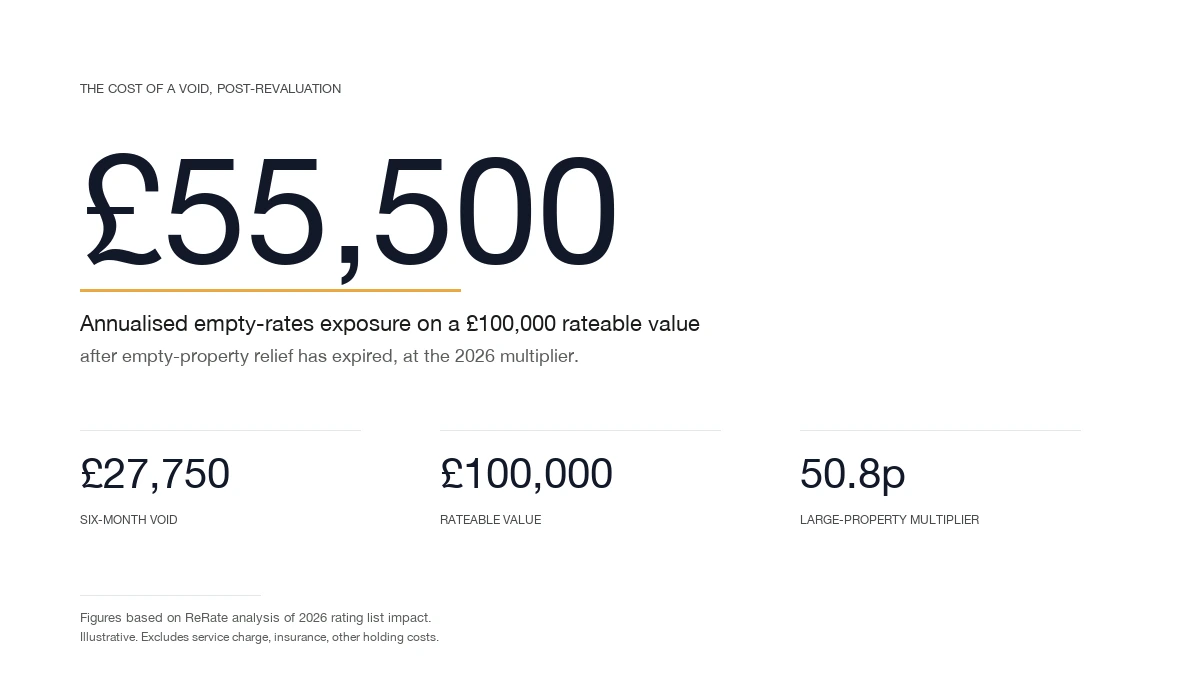

Under the 2026 multipliers that is not a small number.

The ReRate analysis published late last year put the exposure at roughly £55,500 per annum on a property with a £100,000 rateable value, once relief has been exhausted. A six-month void on the same property costs roughly £27,750 before a single other holding cost is counted. Properties crossing the £500,000 rateable value threshold jump into the new large-property multiplier band and the marginal cost curve gets worse, not better.

“Just leaving it empty” is not a strategy any more. It is a slow drip on your balance sheet with a new and much larger meter attached.

Where VacatAd sits in this picture

Because the law now so clearly distinguishes legal entitlement from practical activity, the question for a landlord holding a void is not “how do I look occupied?” It is “who is the lawful occupier here, and does their occupation meet the rateable-occupation test on its own terms?”

That is precisely what VacatAd is built to answer. Our model places a genuine beneficial occupier into the premises under a properly-constituted tenancy, with real business purpose via local advertising delivered through a plug-and-play WiFi unit. The occupier holds legal entitlement. The occupier benefits from the use. The test is satisfied on its own facts, not through a paperwork fiction. That is the space the 2025 Principled judgment carved out, and that Robinson Webster reinforces from the other direction.

The symmetry worth noting

The same reasoning that put £220,000 on Robinson Webster's desk is the reasoning that validates a properly-structured beneficial occupation arrangement. The courts are telling landlords to take legal form seriously. We do.

What to do this month

Three things are worth a morning of your time before May ends.

First, audit every unit that currently sits empty and every unit whose tenant is in or approaching a formal insolvency process. Note the lease status, the surrender position and the occupation history. That is now the most important piece of paper in your rates file.

Second, run the post-revaluation numbers on each void. Use the actual 2026 rateable value, the correct multiplier, and the date your empty relief runs out. Do not rely on last year's figures.

Third, decide what you want to do with the units that come out of that exercise looking expensive. For most landlords, two categories will emerge: units where re-letting is the realistic path, and units where the void will run longer than the market is prepared to accept. The second group is the VacatAd conversation.

If you would like us to run the numbers on a specific asset, we are on hand.

The information in this piece is general guidance on UK business rates and is not tax, legal or valuation advice. Specific mitigation strategies should be reviewed against your portfolio by a qualified rating surveyor and your advisers.

Map your voids against the new multipliers

Use the calculator to see your 2026 exposure per asset, or talk to us about where a properly-constituted beneficial occupation fits your portfolio.

Try the calculator Get in touch